For around three years, iFood has been offering financial services — such as lines of credit — to restaurants, operating as a digital bank that is now launching its new brand: iFood Pago.

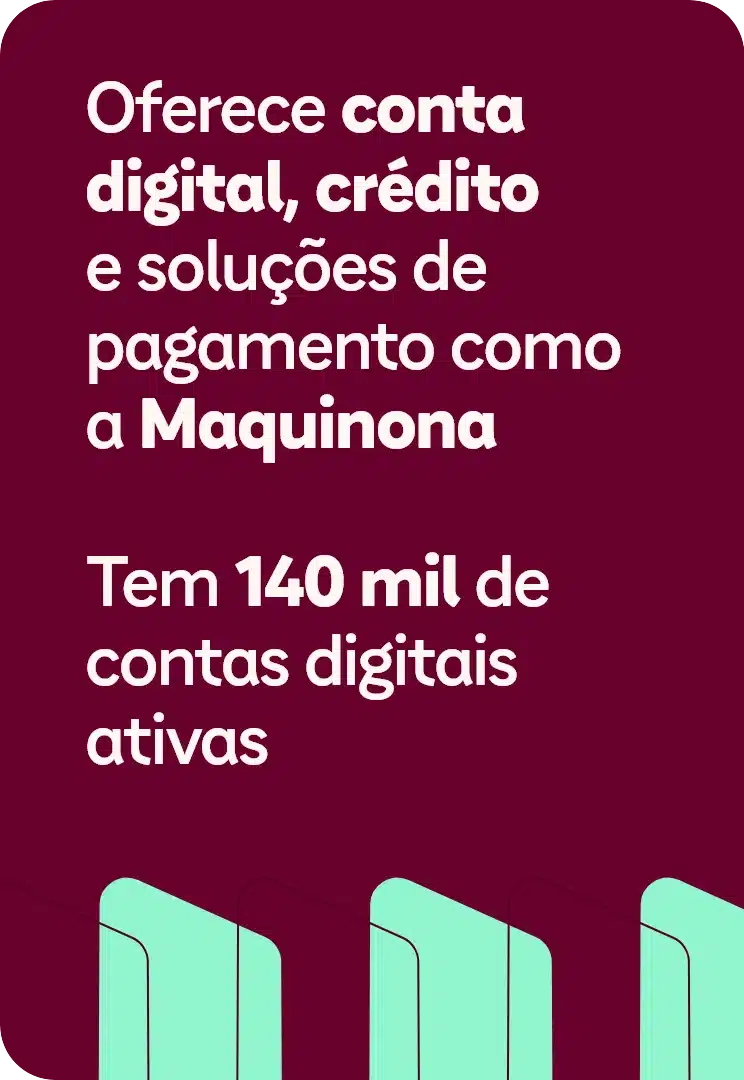

O iFood Paid is the restaurant's bank: it offers digital accounts and payment methods and facilitates access to credit to improve the business's financial management and encourage its growth. Based on transaction data from these partners, it also creates tailored financing lines for each one.

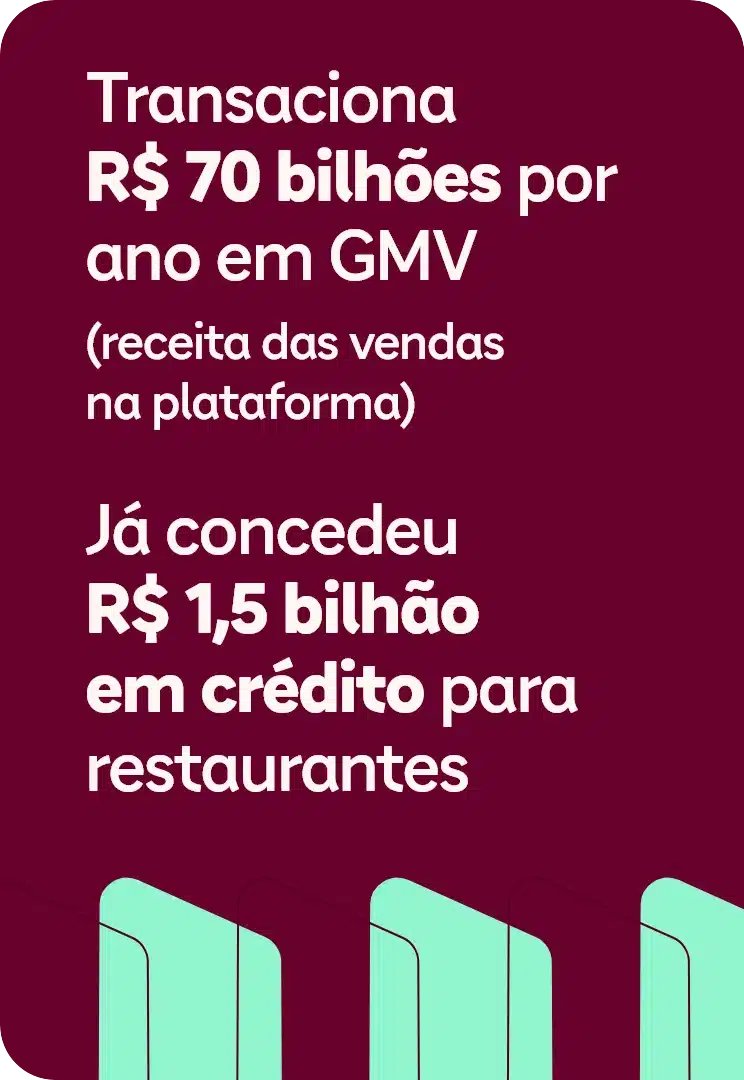

Today, this digital bank has more than 140 thousand active accounts, transacts R$ 70 billion per year in GMV (Gross Merchandise Value, the revenue generated from sales on the platform) and has already granted R$ 1.5 billion in credit to entrepreneurs.

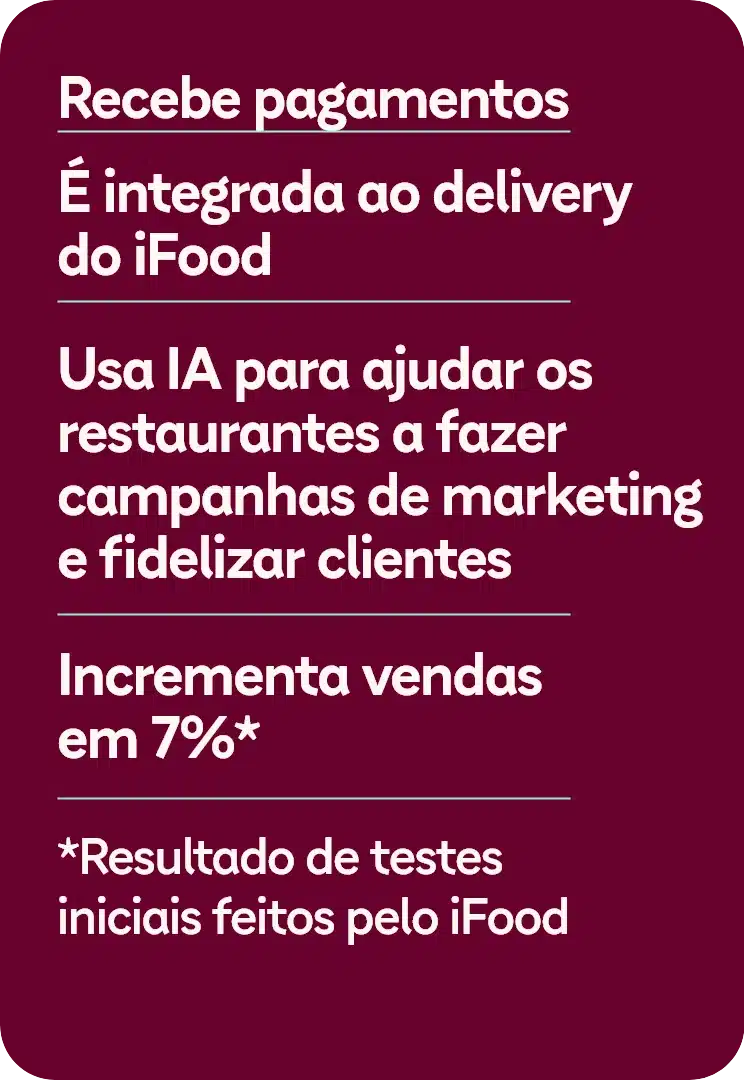

One of the new features of iFood Pago is Maquinona, which comes with the difference of receiving payments in an integrated manner with iFood delivery and using artificial intelligence to help entrepreneurs carry out marketing campaigns to capture and retain customers – both on the app like in the salon.

The expectation is to have around 5,000 Maquinonas on the market in the coming months and 50,000 restaurants adopting this tool by March 2025.

In an interview with iFood News, Bruno Henriques, CEO of iFood Pago, reveals more details about iFood Pago and how its solutions use technology to help restaurants grow.

iFN – iFood has been in the food market for 13 years. How did the company use this expertise to identify restaurants' pain points and create iFood Pago solutions?

The restaurant’s biggest pain is growing. Small entrepreneurs learn how to make good food, open a cool restaurant, and win over customers. But the difficulty is what to do for the business to grow and prosper.

In this sense, iFood Pago comes to help in two ways: with financial products and services and, mainly, with data.

By offering credit, we finance good restaurants, those that want to grow but, to do so, need to expand the room to have more tables, for example. Credit makes this type of investment viable in order to grow.

Additionally, iFood Pago helps with data. In the 13 years that we have been in the market, restaurants have always shown a desire to have access to customer data to better understand their consumption behavior, to know if the person who entered the restaurant has already ordered delivery and how it is possible to retain their loyalty. .

This is a sector that lacks data. Therefore, iFood Pago wants to help these entrepreneurs identify who their customers are by offering structured data so that they can, for example, offer a gift when they see that that person has already consumed five times that month. Or send a notification because she hasn't been to the restaurant in a while.

iFN – How does iFood Pago want to differentiate itself from digital banks?

The difference between iFood Pago is that it is a bank focused on the food ecosystem, with specific financial products for this type of entrepreneur. Our digital account was designed to serve restaurant owners. iFood Pago wants to offer financial products that meet the needs of these entrepreneurs.

iFood, today, brings together 350 thousand restaurants, 250 thousand delivery people and 50 million customers. We know this ecosystem very well and have a close relationship. So we can offer an account made for those who have a restaurant, to help entrepreneurs manage their business and grow.

An example: the digital account will have a receivables calendar to organize the restaurant's financial life, which is a big pain. And it integrates payment methods, whether via WhatsApp, a machine or the iFood app.

These are solutions that were born through data, which is our asset and which will help these businesses function even better. These are theses that we have been testing for around three years, they have gained ground and are now solid.

Another difference is that iFood Pago's financial services connect online and offline businesses. The customer goes to the restaurant, pays at Maquinona, gives their consent and, thus, the establishment has access to their consumption data, both in the iFood app and in the salon.

iFN – What is Maquinona and how does it use AI to do marketing?

Maquinona is not just a means of payment. It also brings data to entrepreneurs. If the customer is in the salon, for example, when paying, they can give consent to share their iFood data with that restaurant.

With this unified data, entrepreneurs have a better idea of the customer's profile and consumption behavior and can create specific actions to build customer loyalty. With Maquinona, the restaurant gains more autonomy to create marketing campaigns.

Using this CRM [customer relationship management] tool, the restaurant can trigger notifications, create marketing campaigns, and run its loyalty program. And you can use the iFood app to send a coupon, a promotion.

iFood uses artificial intelligence a lot to understand who our customers are and what they like to eat most. Maquinona uses this data and AI to bring insights to the restaurant.

It can show how many people in the surrounding area like food that is on your menu but have never purchased from the restaurant. If your price is well above the average in the region. Or bring ideas of what needs to be offered, such as a different burger, to better explore the market in that area.

This is data and insights to help restaurants grow, both by bringing in customers and remodeling the menu.

iFN – How will iFood Pago help restaurants grow?

It's already helping. In the first test we carried out, we saw that restaurants that used Maquinona increased sales by 7%. And that entrepreneurs who received credit from iFood grew 20% more than those who did not receive it.

iFood Pago's financial products are effectively aimed at the growth of restaurants. Now, these entrepreneurs have a partner who invests in them so they can grow.

In this sense, the big difference is that banks cannot know who this restaurant owner is. We know. We know it is selling well, we have data on the behavior and performance of this restaurant on iFood.

This allows us to grant credit more assertively. Other banks may find it risky to give credit to this entrepreneur. Regardless of whatever problem the restaurant owner has, we don't just look at that. If the restaurant is doing well and has been our partner for a long time, we just have to give it credit for growth.

iFN – What is your big dream with iFood Pago?

Our big dream is to be the bank and payment method for the food sector in Brazil. We want to bring data and intelligence to restaurants, reduce the cost of food in the chain and grow.

Our prediction is that, in the first fiscal year, iFood Pago generates revenue of R$ 1 billion. We believe that, as a business, iFood Pago has the potential to be the size of iFood and make the company double its size. This is our dream.